How much can I sell a mortgage note for?

Table Of Contents

Legal Considerations When Selling a Mortgage Note

It is crucial to be aware of the legal considerations when selling a mortgage note to ensure a smooth and lawful transaction process. One primary aspect to keep in mind is verifying the validity of the mortgage note and confirming that all terms and conditions are accurately documented. This includes reviewing the original loan agreement, payment schedule, interest rates, and any other relevant provisions to prevent any discrepancies or disputes during the sale.

Moreover, seeking legal advice from a qualified professional before finalizing the sale of a mortgage note is highly recommended. Legal experts can offer valuable insights on the necessary steps to take, potential risks to consider, and ensure that the transaction adheres to all legal requirements and regulations. By proactively addressing legal considerations and obtaining expert guidance, sellers can mitigate the risk of complications or legal challenges that may arise in the future concerning the mortgage note sale.

Ensuring Compliance with Regulations and Contracts

As you navigate the process of selling a mortgage note, it is imperative to meticulously adhere to all legal regulations and contractual agreements in place. Failure to comply with these obligations can lead to complications, disputes, and potential legal ramifications. Thus, before proceeding with the sale of your mortgage note, it is recommended to review and understand the terms outlined in the contract to ensure a smooth and legally sound transaction.

Furthermore, contracting a legal professional specializing in real estate transactions can provide invaluable guidance and assistance in navigating the intricate legal landscape surrounding the sale of a mortgage note. By seeking expert advice, you can mitigate risks, avoid potential pitfalls, and ensure that all legal requirements are met. Ultimately, prioritizing compliance with regulations and contracts will not only facilitate a successful sale but also safeguard your interests throughout the transaction.

Tax Implications of Selling a Mortgage Note

When contemplating the sale of a mortgage note, it is crucial for sellers to understand the tax implications associated with such transactions. Selling a mortgage note may result in capital gains taxes, which are levied on the profit made from the sale. The amount of tax owed is determined by the length of time the note has been held, with notes sold within a year classified as short-term capital gains and taxed at ordinary income rates, while notes held for over a year are subject to long-term capital gains tax rates.

In addition to capital gains tax, sellers must also consider the potential impact of depreciation recapture tax. This tax is applicable if the property securing the note has been depreciated by the seller. Upon selling the mortgage note, the seller may be required to pay depreciation recapture tax on the portion of the gain attributed to the depreciation taken on the property. Understanding these tax obligations is essential for sellers to accurately assess the profitability of selling their mortgage notes.

Understanding Capital Gains and Tax Obligations

When selling a mortgage note, it is important to be aware of the potential capital gains and tax implications that may arise from the transaction. Capital gains are the profits realized from the sale of an asset, in this case, the mortgage note. The amount of capital gains you incur will depend on various factors, including the original purchase price of the note, the selling price, and any expenses incurred during the sale process.

In terms of tax obligations, selling a mortgage note can trigger tax liabilities that you should be prepared for. Capital gains tax is typically assessed on the profit made from the sale of the note. Depending on how long you have held onto the note before selling it, you may be subject to short-term capital gains tax rates (for notes held less than a year) or long-term capital gains tax rates (for notes held over a year). It is advisable to consult with a tax professional or financial advisor to understand your specific tax obligations and how best to manage them when selling a mortgage note.

Timing the Sale of Your Mortgage Note

When contemplating the timing of selling your mortgage note, it is crucial to gauge the current market conditions and interest rates. Opting to sell during a period where interest rates are low can potentially entice more buyers and result in a more lucrative sale. It is prudent to keep a close watch on economic indicators and market trends to identify the optimal window for selling your mortgage note.

Another factor to consider when deciding the timing of your mortgage note sale is the financial position of potential buyers. During times of economic stability and growth, buyers may be more inclined to invest, leading to a higher demand for mortgage notes. Conversely, in times of economic uncertainty, buyers may be more cautious, impacting the potential offers you receive for your mortgage note. By staying informed about economic conditions, you can strategically time the sale of your mortgage note to maximize your profits.

Identifying Optimal Market Conditions for a Sale

To identify optimal market conditions for selling a mortgage note, it is crucial to monitor interest rates and the overall economic climate. When interest rates are low, the value of a mortgage note tends to increase as buyers are willing to pay a premium for higher-yielding assets. Additionally, a strong economy with low unemployment rates may attract more investors looking for stable returns, thus creating a favorable market for selling mortgage notes.

Furthermore, keeping an eye on the real estate market can also provide insights into the optimal time to sell a mortgage note. In a booming real estate market, property values tend to rise, which can positively impact the value of a mortgage note. Conversely, during a market downturn, it might be advisable to hold onto the note until conditions improve to maximize potential returns. By staying attuned to these market conditions, sellers can strategically time the sale of their mortgage note for maximum profitability.

FAQS

Can I sell a mortgage note for more than its original value?

Yes, you can potentially sell a mortgage note for more than its original value, especially if the property’s value has increased since the note was created.

How is the selling price of a mortgage note determined?

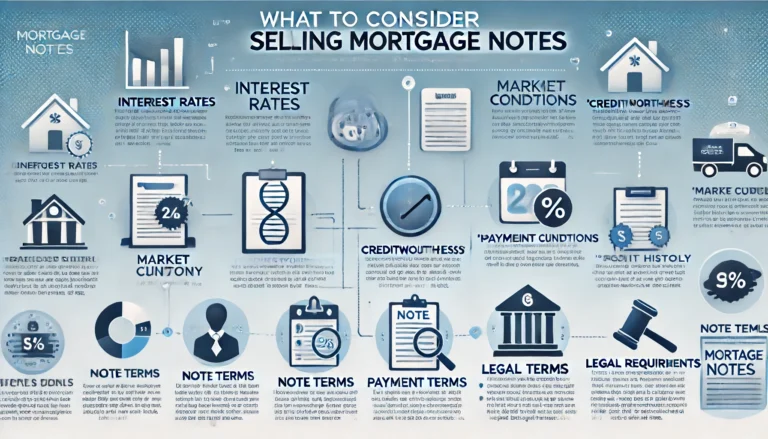

The selling price of a mortgage note is typically influenced by factors such as the remaining balance, interest rate, payment history, property value, and current market conditions.

Are there any fees or costs associated with selling a mortgage note?

Yes, there may be fees involved in selling a mortgage note, such as closing costs, servicing fees, and potentially legal fees depending on the complexity of the transaction.

Is it possible to negotiate the selling price of a mortgage note?

Yes, it is possible to negotiate the selling price of a mortgage note with potential buyers or investors to reach a mutually beneficial agreement.

How long does it usually take to sell a mortgage note?

The time it takes to sell a mortgage note can vary depending on factors such as market demand, the complexity of the note, and the efficiency of the transaction process, but it typically ranges from a few weeks to a few months.